|

Amendment to the Companies (Corporate Social Responsibility Policy) Rules, 2014 and Schedule VII of the Companies Act, 2013

|

| As per the Companies (Corporate Social Responsibility Policy) Rules, 2014, the CSR Policy of a company shall include a list of CSR projects or programs which a company plans...More |

|

As per the Companies (Corporate Social Responsibility Policy) Rules, 2014, the CSR Policy of a company shall include a list of CSR projects or programs which a company plans to undertake as specified in Schedule VII of the Companies Act, 2013 (“Act”) and the expenditure, excluding activities undertaken in pursuance of the normal course of business of a company. |

| The MCA vide Notification No. G.S.R. 526(E) dated August 24, 2020 introduced the Companies (Corporate Social Responsibility Policy) Amendment Rules, 2020 wherein it was stated that any company engaged in the research and development activity of a new vaccine, drugs and medical devices in their normal course of business may undertake the research and development activity of the new vaccine, drugs and medical devices related to COVID-19 as expenditure incurred for CSR activities for the financial years 2020-21, 2021-22 and 2022-23 subject to the conditions that: |

|

(i) |

such research and development activities shall be carried out in collaboration with any of the institutes or organisations mentioned in item (ix) of Schedule VII to the Act. |

|

(ii) |

details of such activity shall be disclosed separately in the annual report on CSR included in the Board’s report of such companies. |

|

Further, the MCA has vide Notification No. G.S.R. 525(E) dated August 24, 2020 amended Schedule VII of the Act by substituting item (ix) of the said schedule with the following: |

|

a. |

Contribution to incubators or research and development projects in the field of science, technology, engineering and medicine, funded by the Central Government or State Government or Public Sector Undertaking or any agency of the Central Government or State Government; and |

|

b. |

Contributions to public funded universities, Indian Institute of Technology (IITs), National Laboratories and Autonomous Bodies established under Department of Atomic Energy (DAE), Department of Science and Technology (DST), Department of Biotechnology (DBT), Department of Pharmaceuticals, Ministry of Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homoeopathy (AYUSH), Ministry of Electronics and Information Technology (MEITY) and other bodies, namely Defense Research and Development Organisation (DRDO), Indian Council of Agricultural Research (ICAR), Indian Council of Medical Research (ICMR), Council of Scientific and Industrial Research (CSIR), engaged in conducting research in science, technology, engineering and medicine aimed at promoting Sustainable Development Goals (SDGs). |

|

|

Companies to place extract of the Annual Returns (Form MGT-9) on their website

|

| The MCA finally notified the long-awaited amendment in Section 92 of the Act relating to extract of annual return vide Notifications Number S.O. 2920(E) dated...More |

|

The MCA finally notified the long-awaited amendment in Section 92 of the Act relating to extract of annual return vide Notifications Number S.O. 2920(E) dated August 28, 2020 and G.S.R. 538(E) dated August 28, 2020 by amending the Companies (Management and Administration) Rules, 2014. Now, if a company has its own website, the annual return can be uploaded on the website and its extract will not be required to be attached with the Board’s report in Form No. MGT-9, in case the web link of such annual return has been disclosed in the Board’s report. Where a company has no website, it will continue to attach the extract of annual return with the Board’s report in Form No. MGT-9.

|

|

It is important to note that while the enabling provisions under Section 92 to provide for extract of Form MGT-9 has been omitted but the Rules continue to provide for the same.

|

|

|

Director’s minimum residency requirement for 182 days relaxed for financial year 2020-21

|

| Relaxation under Section 149 of the Act was earlier granted vide General Circular No. 11/2020 where the requirement for minimum residency in India for a period of at least 182...More |

|

Relaxation under Section 149 of the Act was earlier granted vide General Circular No. 11/2020 where the requirement for minimum residency in India for a period of at least 182 (one hundred and eighty two) days by at least one director of every company would not be treated as a non-compliance for the financial year 2019-20. This relaxation has now been extended for the financial year 2020-21 as well vide General Circular No. 36/2020 dated October 20, 2020.

|

|

One time resolution for ease of fund raising through Qualified Institutional Buyers

|

| The MCA vide Notification No. G.S.R.642(E) dated October 16, 2020 has notified the Companies (Prospectus and Allotment of Securities) Amendment Rules, 2020 to...More |

|

The MCA vide Notification No. G.S.R.642(E) dated October 16, 2020 has notified the Companies (Prospectus and Allotment of Securities) Amendment Rules, 2020 to further amend the Companies (Prospectus and Allotment of Securities) Rules, 2014. The amendment is brought under Rule 14 which deals with private placement in which a company may make an offer or invitation to subscribe to securities through issue of a private placement offer letter in Form PAS-4. Through this amendment, the proviso has been inserted under Rule 14 to provide that in case of offer or invitation of any securities to qualified institutional buyers, it shall be sufficient if the company passes a previous special resolution only once in a year for all the allotments to such buyers during the year.

|

|

Extension of the ‘Companies Fresh Start Scheme, 2020’ and ‘LLP Settlement Scheme, 2020’

|

| The MCA had earlier introduced a scheme known as the Companies Fresh Start Scheme, 2020, which was valid from April 1, 2020 to September 30, 2020 to enable companies to file their... More |

|

The MCA had earlier introduced a scheme known as the Companies Fresh Start Scheme, 2020, which was valid from April 1, 2020 to September 30, 2020 to enable companies to file their belated returns without any penalty or prosecution. This scheme has now been extended till December 31, 2020 vide General Circular No. 30/2020 dated September 28, 2020.

|

|

A similar scheme called the LLP Settlement Scheme, 2020, which was valid from April 1, 2020 to September 30, 2020 to reduce the compliance burden faced by limited liability partnerships in light of the COVID-19 pandemic has also been extended till December 31, 2020 vide General Circular No. 31/2020 dated September 28, 2020.

|

|

|

Extension of timelines

|

| (a) MCA provides clarification on extension of timelines for conducting the Annual General...More |

|

(a)

|

MCA provides clarification on extension of timelines for conducting the Annual General Meeting (“AGM”)

|

|

|

The MCA in its Circular No. 20/2020 dated May 05, 2020 stated that AGMs could be conducted through video conferencing or through other audio-visual means. Further, companies who were unable to hold their AGMs through such means were advised to make an application to the concerned Registrar of Companies (“ROC”) for extension of conducting the AGM.

|

|

|

The MCA has vide Circular No. 28/2020 dated August 17, 2020 reiterated that companies unable to hold their AGM for the financial year ending on March 31, 2020 to make applications (in form GNL-1) on or before September 29, 2020 to the ROC for seeking an extension for holding their AGM. MCA further advised to ROCs to consider all such applications liberally in view of the hardships faced by the stakeholders and to grant extension for the period as applied for (up to 3 (three) months) in such applications.

|

|

(b)

|

Extension of timelines for companies to conduct their EGMs through VC or OAVM

|

| |

The MCA, in continuation of General Circulars No. 14/2020, 17/2020 and 22/2020, has vide Circular No. 33/2020 dated September 28, 2020 extended the relaxation allowing companies to conduct their extraordinary general meetings through video conference or through other audio-visual means and transact items through postal ballot in accordance with the framework provided in the aforesaid circulars up to December 31, 2020.

|

|

|

Please refer to our update in relation to Circular 14/2020 and Circular 17/2020 here.

|

|

(c)

|

MCA further extends board meetings to be held via video conference on restricted matters till December 31, 2020

|

|

|

The MCA vide the Companies (Meetings of Board and its Powers) Amendment Rules, 2020 dated March 19, 2020 and the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2020 dated June 23, 2020 had permitted companies to conduct board meetings to discuss matters provided under Section 173 (2) of the Act read with Rule 4 of the Companies (Meetings of Board and its Powers) Rules, 2014 such as approval of the annual financial statements, Board’s report, approval of prospectus, the audit committee meetings for consideration of accounts, approval of matters relating to amalgamation, merger, demerger, acquisition and takeover, through video conferencing or other audio-visual means till September 30, 2020.

|

|

|

The MCA vide Notification No. G.S.R. 590(E) dated September 28, 2020 has introduced the Companies (Meetings of Board and its Powers) Third Amendment Rules, 2020 which has extended the timelines for conducting board meetings to discuss the above restricted matters from September 30, 2020 to December 31, 2020.

|

|

(d)

|

Extension of timelines for filing forms relating to creation or modification of charges

|

|

|

The MCA had earlier through General Circular No. 23/2020 introduced a scheme for relaxation of timelines for filing forms relating to creation or modification of charges (i.e. forms CHG-1 and CHG-9) under the Act. It has now, vide General Circular No. 32/2020 dated September 28, 2020, extended the aforesaid scheme till December 31, 2020.

|

|

|

Dates referring to “September 30, 2020” and “October 1, 2020” under the previous General Circular No. 23/2020 have been substituted with “December 31, 2020” and “January 1, 2021” accordingly.

|

|

|

Please refer to our newsletter update in relation to General Circular No. 23/2020 here.

|

|

(e)

|

Extension of additional 3 (three) months for enrolment by Independent Directors in the database

|

|

|

As per Rule 6 of the Companies (Appointment and Qualifications of Directors) Rules, 2014 every existing independent director is required to apply for registration/listing in an online data bank maintained by the Indian Institute of Corporate Affairs within 10 (ten) months from the date of commencement of the Companies (Appointment and Qualification of Directors) Fifth Amendment Rules, 2019 i.e. December 1, 2019.

|

|

|

The MCA vide Notification No. G.S.R. 589 (E) dated September 28, 2020 has extended the deadline for enrolment in the online database to 13 (thirteen) months from December 1, 2019 i.e. by December 31, 2020.

|

|

Relaxation of additional fees and extension of last date of filing of Form CRA-4 for FY 2019-20

|

| The MCA has vide General Circular No. 29/2020 dated September 10, 2020 stated that if the cost audit report for the financial year 2019-2020 has been submitted by the cost...More |

| The MCA has vide General Circular No. 29/2020 dated September 10, 2020 stated that if the cost audit report for the financial year 2019-2020 has been submitted by the cost auditor to board of directors by November 30, 2020 then it shall not be considered as a violation of the timeline period of 180 (one hundred and eighty) days from the close of financial year as per the Companies (Cost Records and Audit) Rules, 2014. |

|

Accordingly, the e-Form CRA-4 (Form for Filing Cost Audit Report with Central Government) for the financial year ending on March 31, 2020 can also be filed within 30 (thirty) days from the date of receipt of the copy of the cost audit report by the company. However, where the company has availed an extension of time for holding annual general meeting, then the e-form CRA-4 can be filed within the extended period for filing financial statements under Section 137 of the Act (Copy of Financial Statement to be Filed with Registrar).

|

|

Extension of the period for the creation of deposit repayment reserve, investment of debentures under the provisions of Section 72(2)(c) of the Act

|

|

MCA vide Circular No. 34/2020 dated September 29, 2020, issued a circular for extension of the period for the creation of deposit repayment reserve, investment...More

|

|

MCA vide Circular No. 34/2020 dated September 29, 2020, issued a circular for extension of the period for the creation of deposit repayment reserve, investment of debentures under the provisions of Section 72(2)(c) of the Act. In continuation of General Circular No. 11/2020 dated March 24, 2020, MCA and keeping in view the requests received from various stakeholders seeking an extension of time for compliance of the subject requirements on account of COVID-19, the time in respect of matters referred to in Paras V, VI of the original circular has been extended up to December 31, 2020. All other requirements shall remain unchanged. Accordingly, the time is extended for the creation of a deposit repayment reserve of 20% under Section 73(2)(C) of the Act and to invest or deposit 15% of the amount of debentures under Rule 18 of Companies (Share Capital and Debentures) Rules 2014 up to December 31, 2020.

|

|

UPDATES UNDER FEMA

|

|

Introduction of the Foreign Exchange Management (Non-debt Instruments) (Third Amendment) Rules, 2020

|

|

The Ministry of Finance, vide Notification dated October 17, 2019, had introduced the Foreign Exchange Management (Non-debt Instruments) Rules, 2019...More

|

|

The Ministry of Finance, vide Notification dated October 17, 2019, had introduced the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (“NDI Rules”), superseding the erstwhile Foreign Exchange Management (Transfer and Issue of Security by a Person Resident outside India) Regulations, 2017 and the Foreign Exchange Management (Acquisition and Transfer of Immovable Property in India) Regulations, 2018. The introduction of the NDI Rules resulted from a power shift from the Reserve Bank of India (“RBI”) to the Central Government, with regard to drafting of regulations for non-debt instruments (while the RBI was concerned with drafting of regulations for debt instruments). The NDI Rules govern the foreign investment regime in India.

|

|

Thereafter, on July 27, 2020, the Ministry of Finance introduced the Foreign Exchange Management (Non-debt Instruments) (Third Amendment) Rules, 2020, further amending the NDI Rules (“NDI Amendment Rules”) and giving administrative powers to the RBI in order to ensure effective implementation of the NDI Rules. This is aimed at reducing timelines and make the approval process faster and more effective, however, the powers granted to the Central Government to frame regulations in relation to non-debt instruments continue to remain intact. The key highlights of the NDI Amendment Rules are as follows:

|

-

The NDI Amendment Rules provide RBI with administrative powers and have removed the requirement of Central Government consultation, providing RBI more freedom to act on certain matters. Pursuant to the said amendment, RBI is empowered to administer the NDI Rules, and while doing it, the RBI has the power to issue such directions, circulars, instructions, clarifications necessary for effective implementation of the NDI Amendment Rules, without consulting the Central Government.

-

As per the NDI Rules, RBI was required to consult the Central Government for certain matters. With the introduction of the NDI Amendment Rules, this requirement has been done away with and now RBI can permit (i) investments in India by persons resident outside India with respect to matters not already covered in the NDI Rules and/or (ii) an Indian entity/investment vehicle/venture capital fund/firm/association of persons/proprietary concern to receive any investment in India from a person resident outside India or to record such investment, with respect to matters not already covered in the NDI Rules, without consulting the Central Government. For purposes of clarity, wherever Government approval is required to be sought for any foreign investments as per the NDI Rules, such approval will still be required to be sought from the Department for Promotion of Industry and Internal Trade (DPIIT) and/or any of the prescribed ministry/department of the Government of India.

-

With respect to foreign investments in civil aviation sector, DPIIT vide Press Note No. 2 (2020 Series) dated March 19, 2020 amended the foreign direct investment policy in order to attract more non-resident Indians investments and in view of the Government’s proposed strategic disinvestment from Air India Limited (Air India). Accordingly, foreign investment in Air India was permitted by non-resident Indians up to 100% under automatic route, provided that substantial ownership and effective control of Air India continues to be vested with Indian nationals.

|

|

Further, in order to align with Schedule XI of Aircraft Rules 1937, the NDI Amendment Rules provide that an Air Operator Certificate to operate Scheduled Air Transport Services (including Domestic Scheduled Passenger Airline or Regional Air Transport Service) can also be granted to a body corporate (in addition to a company) subject to the conditions that (i) it is registered and has its principal place of business within India; (ii) the Chairman and at least 2/3rds of its directors are citizens of India; and (iii) it’s substantial ownership and effective control is vested in Indian nationals.

|

|

Accordingly, the NDI Amendment Rules have notified the changes brought in the air transport services sector under the said Press Note No. 2 (2020 Series).

|

|

RBI notifies the Foreign Exchange Management (Export and Import of Currency) (Amendment) Regulations, 2020

|

|

The RBI, has vide Notification dated August 11, 2020, introduced the Foreign Exchange Management (Export and Import of Currency) (Amendment) Regulations, 2020...More

|

|

The RBI, has vide Notification dated August 11, 2020, introduced the Foreign Exchange Management (Export and Import of Currency) (Amendment) Regulations, 2020, which aims to ease the norms for export and import of currency/currency notes. The said amendment, effective from August 18, 2020, seeks to amend the Foreign Exchange Management (Export and Import of Currency) Regulations, 2015 (“Regulations”) i.e. the principal legislation that provides for the export from and import into India, of currency/currency notes.

|

The said amendment provides for omission of the proviso to Regulation 3(1) of the Regulations, which dealt with the rules for import or export of currency/current notes in India. The said proviso empowered the RBI to allow, on being satisfied that it is necessary to do so, a person to take or send out of India or bring into India, Indian currency notes and/or those of RBI, subject to such terms and conditions stipulated by the RBI.

|

|

Further, pursuant to the said amendment, the omitted provision has been now introduced as a new and independent Regulation 9, which provides for RBI’s power to permit export or import of currency. It provides that the RBI, on an application made to it, can grant permissions to take or send out of India to any country or bring into India from any country currency notes of Government of India and/or of RBI, subject to terms and conditions specified by the RBI. The RBI must also determine and be satisfied that such import or export of Indian currency is necessary.

|

|

RBI exempts venture capital fund companies from Section 45-IA and 45-IC of the Reserve Bank of India Act, 1934

|

|

The RBI vide its Notification RBI/2020-21/12 DOR (NBFC).CC.PD.No.115/03.10.001/2020-21 dated July 10, 2020 exempted venture capital fund companies holding a certificate of...More

|

|

The RBI vide its Notification RBI/2020-21/12 DOR (NBFC).CC.PD.No.115/03.10.001/2020-21 dated July 10, 2020 exempted venture capital fund companies holding a certificate of registration obtained under Section 12 of the Securities and Exchange Board of India Act, 1992 and not holding or accepting public deposit from the provisions of Section 45-IA which deals with the requirement of registration and net owned fund and 45-IC which specifies reserve fund of the RBI Act, 1934. Further, RBI also exempts those venture capital fund companies from the applicability of guidelines issued by the Bank for NBFCs. Further, consequent upon the repeal of Securities and Exchange Board of India (Venture Capital Funds) Regulations, 1996 and enactment of Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012, it has been decided to substitute the word “Venture Capital Fund Companies” with “Alternative Investment Fund Companies”, in exercise of the powers conferred under Section 45NC of RBI Act, 1934.

|

|

Increase in FDI cap limit for defence sector

|

|

On September 17, 2020, the DPIIT issued a Press Note 4 (2020 Series) (PN 4/2020) increasing the foreign direct investment limit in the defence sector from 49% to 74%...More

|

|

On September 17, 2020, the DPIIT issued a Press Note 4 (2020 Series) (PN 4/2020) increasing the foreign direct investment limit in the defence sector from 49% to 74% under the automatic route.

|

|

The PN 4/2020 also prescribes that the foreign investment in the defence sector would be subject to scrutiny on the grounds of national security and the government reserves the right to review any foreign investment in the sector that affects or may affect national security.

|

|

Further, as per the earlier FDI regime, infusion of fresh foreign investment up to 49% (earlier cap) in a company not seeking industrial license resulting in change in the ownership pattern or transfer of stake by existing investor to new foreign investor required government approval. As per the PN 4/2020, infusion of fresh foreign investment up to 49% in a company not seeking industrial license or which already has government approval for FDI in defence will need to mandatorily submit a declaration with the Ministry of Defence in case of change in equity/shareholding pattern or transfer of stake by existing investor to new foreign investor for FDI up to 49%, within 30 days of such change. Government approval will be required for raising FDI beyond 49% in such companies. The other conditions under the FDI remain unchanged.

|

|

Government releases the new Consolidated Foreign Direct Investment Policy 2020

|

|

On October 28, 2020, the Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry (“DPIIT”), released the new version of the Consolidated Foreign Direct Investment...More

|

|

On October 28, 2020, the Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry (“DPIIT”), released the new version of the Consolidated Foreign Direct Investment (FDI) Policy (“Consolidated FDI Policy 2020”), after a long 3 (three) years gap. The Consolidated FDI Policy 2020 incorporates all the foreign investment related changes and measures adopted by the government recently. The policy document states that the FDI Policy 2020 became effective from October 15, 2020. The copy of the Consolidated FDI Policy 2020 can be accessed here.

|

|

The Consolidated FDI Policy 2020 incorporates the restrictions notified earlier this year on foreign direct investment for curbing opportunistic takeover/acquisition of Indian companies by entities and/or citizens (having beneficial ownership) of neighboring countries sharing land border with India, including China and permitting such investments to be made only through the government approval route. The Consolidated FDI Policy 2020 also captures the government’s decision of permitting FDI up to 26% through government approval route, for entities engaged in uploading or streaming of news and current affairs through digital media as well as liberalizations introduced for various sectors, such as defence, coal mining, digital news, contract manufacturing and single-brand retail trading.

|

|

Government issues clarification on the FDI Policy for uploading/streaming of news and current affairs through digital media

|

|

The DPIIT had released a Press Note No. 4 (2019 Series) dated September 18, 2019 (PN 4/2019), under which “digital media” was introduced for the first time under the ambit of FDI Policy...More

|

|

The DPIIT had released a Press Note No. 4 (2019 Series) dated September 18, 2019 (PN 4/2019), under which “digital media” was introduced for the first time under the ambit of FDI Policy, permitting FDI in ‘uploading/streaming of News & Current Affairs through Digital Media’ up to 26% under government approval route. Thereafter, on December 5, 2019, the Ministry of Finance notified the Foreign Exchange Management (Non-debt Instruments) (Amendment) Rules, 2019 (FEMA NDI Rules) incorporating the above mentioned changes introduced in relation to digital media, in order to give effect to the FDI regime under PN 4/2019.

|

|

Prior to the introduction of PN 4/2019, the FDI policy did not prescribe any limit in the digital media sector and accordingly, there were many digital media companies in India which had received FDI under automatic route, beyond 26%. Further, neither the PN 4/2019 nor the FEMA NDI Rules defined “news and current affairs”, “digital media”, “uploading” and “streaming” and accordingly, there remained an uncertainty regarding the interpretation and intent of this amendment and inclusion of digital media sector under the FDI Policy. This led to a lot of confusion on the applicability of the restrictions on the media companies as the PN 4/2019 did not clarify which entities will be covered within the ambit of the term ‘digital media’.

|

|

On October 16, 2020, the DPIIT has issued a clarification on various concerns and open issues underlying the FDI regime in digital media sector as prescribed under the PN 4/2019, in response to the various representations from stakeholders to the government seeking clarity on the same.

|

|

Categories of Indian entities covered under PN 4/2019: The FDI restrictions of 26% cap under government approval route shall apply to the following categories of Indian companies in the digital media space:

|

-

digital media entities streaming/uploading news and current affairs on websites, apps or other platforms.

-

news agency which gathers, writes and distributes/transmits news, directly or indirectly, to digital media entities and/or news aggregators.

-

news aggregator, being an entity which, using software of web application, aggregates news content from various sources, such as news websites, blogs, podcasts, video blogs, user submitted links, etc. in one location.

|

|

Sunset Period: All companies that fall within the ambit of PN 4/2019 (as above) have a period of 1 (one) year from the date of issue of the clarification (i.e. by October 15, 2021) to align their shareholding with the 26% FDI cap with government approval. Accordingly, all such companies will have to assess the applicability of the PN 4/2019 and restructure their shareholding in compliance with the 26% limit and seek government approval in compliance with the provisions of the PN 4/2019.

|

|

Responsibility: The clarification states that the responsibility of complying with provisions of PN 4/2019 (such as seeking government approval) shall be on the investee company.

|

|

Additional compliance conditions: The clarification also provides that the majority of the board of directors and chief executive officer (CEO) of investee digital media companies with FDI will have to be Indian citizens and the firms will have to get security nod for all foreign personnel to be deployed for more than 60 (sixty) days in a year by way of appointment, contract or consultancy or in any other capacity for functioning of the entity prior to their deployment. In the event of the security clearance of any foreign personnel being denied or withdrawn for any reasons whatsoever, the investee entity is required to ensure that the concerned person resigns or his/her services are terminated forthwith after receiving such directives from the government.

|

|

Further, the Ministry of Information and Broadcasting on October 16, 2020 stated that it will be considering in the near future to extend the following benefits, presently available to traditional media (print and TV), to such entities also:

|

-

Press Information Bureau (“PIB”) accreditation for its reporters, cameramen, videographers enabling them with better first-hand information and access including participation in official press conference and such other interactions.

-

Persons with PIB accreditation can also avail Central Government Health Scheme benefits and concessional rail fare as per extant procedure.

-

Eligibility for digital advertisements through Bureau of Outreach and Communication.

|

|

Further, the Ministry of Information and Broadcasting also stated that similar to self-regulating bodies in print and electronic media, entities in digital media can form self-regulating bodies for furthering their interests and interaction with the Government.

|

|

Foreign Contribution (Regulation) Amendment Act, 2020

|

|

The Foreign Contribution (Regulation) Act, 2010 (“FCRA”) regulates the acceptance and utilisation of foreign contributions and donations by individuals, associations and companies...More

|

|

The Foreign Contribution (Regulation) Act, 2010 (“FCRA”) regulates the acceptance and utilisation of foreign contributions and donations by individuals, associations and companies to ensure that such contributions, do not adversely affect national security. However, in the recent years, registrations of several organisations have been cancelled by the government due to violations of the basic statutory compliance requirements under the FCRA, such as submission of annual returns and maintenance of proper accounts as well as mis-utilisation of foreign contribution received. On September 29, 2020, the Government of India notified the Foreign Contribution (Regulation) Amendment Act, 2020 (“FCRA Amendment Act”) amending certain provisions of the FCRA. The object of the FCRA Amendment Act is to strengthen the compliance mechanism, enhance transparency and accountability in the receipt and utilisation of foreign contribution and facilitate genuine non-governmental organisations (“NGOs”) or associations who are working for the welfare of the society.

|

|

Some of the changes introduced by the Government regarding the framework for governing foreign contributions include reduction of limit of foreign contribution that can be used for administrative expenses of NGOs from 50% to 20%, restriction on transferability of foreign contributions, mandatory Aadhaar requirement for office bearers of NGOs at the time of registration, power of government to allow suspension of FCRA registration certificate.

|

|

We have briefly summarised below the key changes introduced under the FCRA Amendment Act:

|

|

Prohibition on transfer of foreign contribution: Previously under the FCRA, foreign contribution could not be transferred to any person except to person registered to accept foreign contribution (or person who has obtained prior permission under FCRA to obtain foreign contribution). The FCRA Amendment Act now prohibits transfer of foreign contribution to all person including person registered to accept foreign contribution (or has obtained prior permission under FCRA to obtain foreign contribution).

|

Prohibition to accept foreign contribution by public servants: Under the FCRA, certain persons were prohibited to accept any foreign contribution, such as election candidates, editor or publisher of a newspaper, judges, government servants, members of any legislature and political parties, among others. The FCRA Amendment Act has added “public servants” to this list to widen the ambit of the persons who are restricted from receiving foreign contributions. Public servant includes all persons in service or pay of the government or remunerated in the form of by fees or commission by the government for the performance of any public duty.

|

|

Reduction of limit of foreign contribution that can be used as administrative expenses: The percentage of foreign contributions that can be utilised for meeting administrative expenses has been reduced from the earlier cap of 50% to 20% of the foreign contribution received in a year.

|

|

Power to prohibit foreign contribution recipients from utilising/receiving its funds during pendency of an inquiry: Under the FCRA, if a person accepting foreign contributions is found guilty of violating any provisions of the Act, the unutilised or unreceived foreign contribution could be utilised or received, only with the prior approval of the central government. The FCRA Amendment Act provides that the government may also restrict usage of unutilised foreign contribution for persons who have been granted prior permission to receive such contribution on the basis of a summary inquiry, and pending any further inquiry, the government believes that such person has contravened provisions of the FCRA.

|

|

Mandatory identification requirements – Aadhaar: The FCRA Amendment Act provides that the Central Government may require persons seeking registration/prior permission/renewal under the FCRA to provide Aadhaar number (passport or Overseas Citizen of India card, in case of foreigners) of all their office bearers, directors, key functionaries.

|

|

Inflow of foreign contributions through a single designated bank branch: The FCRA earlier provided that foreign contribution may be received in a single branch of any scheduled bank and more accounts may be opened in other banks for utilisation of the contribution. The FCRA Amendment Act makes it mandatory for all persons receiving foreign contribution to receive foreign contribution in an account designated as "FCRA account", opened with the prescribed branch of the State Bank of India, New Delhi. Further, no funds other than foreign contribution can be received or deposited in the FCRA account. Such person is, however, permitted to open other FCRA accounts in any scheduled bank of their choice for keeping or utilising the received contribution.

|

|

Suspension of registration: The FCRA provided that the central government could suspend the registration of a person for a period, not exceeding 180 days. The FCRA Amendment Act gives the central government the power to suspend the registration certificate of a person for another period of 180 days, in addition to the existing 180 days i.e. up to 360 days.

|

|

Surrender of registration certificate: The FCRA Amendment Act adds a provision allowing the central government to permit a person to surrender their registration certificate, if it is satisfied that such person has not contravened any provisions of the FCRA, and the management of its foreign contribution (and related assets) has been vested in an authority prescribed by the government.

|

|

UPDATES ISSUED BY THE SECURITIES EXCHANGE BOARD OF INDIA (“SEBI”)

|

|

SEBI (Settlement Proceedings) (Amendment) Regulations, 2020

|

| SEBI, vide Notification No. SEBI/LAD-NRO/GN/2020/24 dated July 22, 2020 (“Notification”) has amended inter alia Regulation 15(2)(a) of the Securities and Exchange Board of India...More |

|

SEBI, vide Notification No. SEBI/LAD-NRO/GN/2020/24 dated July 22, 2020 (“Notification”) has amended inter alia Regulation 15(2)(a) of the Securities and Exchange Board of India (Settlement Proceedings) Regulations, 2018, pursuant to which the time period for remittance of the settlement amount (which forms part of the settlement terms) by the applicant has been increased from 15 (fifteen) days to 30 (thirty) days. Additionally, this period of 30 (thirty) days may be extended to 60 (sixty) days, post receipt of an application seeking extension of time within 30 (thirty) days from the date of receipt of notice of demand.

|

|

SEBI issues circular on recording of all types of Encumbrances in Depository system

|

|

SEBI, vide Circular No. SEBI/HO/MRD2/DDAP/CIR/P/2020/137 dated July 24, 2020 (“Circular”), has issued directions for the recording of encumbrances in the depository system...More

|

|

SEBI, vide Circular No. SEBI/HO/MRD2/DDAP/CIR/P/2020/137 dated July 24, 2020 (“Circular”), has issued directions for the recording of encumbrances in the depository system, in light of the requirement for promoters of a company to disclose details of their encumbered shares under SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 2011 (“SAST Regulations”). The Circular inter alia provides for the following:

|

-

Depositories are required to put in place a system for capturing and recording all types of encumbrances, which are specified under Regulation 28(3) of the SAST Regulations.

-

The freeze and unfreeze instructions executed by the Participant for recording all encumbrances will be subject to 100% concurrent audit.

-

The Depository Participant will not facilitate or be a party to any type of encumbrance outside the Depository system as outlined in the Circular.

-

The Depositories are required to implement the provisions of the Circular within 1 (one) month from the date of the Circular.

|

|

Relaxations relating to procedural matters pertaining to issue and listing of Rights Issue

|

|

SEBI had previously, vide circular dated May 6, 2020 granted one-time relaxation from strict enforcement of certain procedural requirements of ICDR Regulations pertaining to rights...More

|

|

SEBI had previously, vide circular dated May 6, 2020 granted one-time relaxation from strict enforcement of certain procedural requirements of ICDR Regulations pertaining to rights issue opening up to July 31, 2020. This update can be accessed from our earlier updates as provided here. SEBI has now, vide circular SEBI/HO/CFD/DIL1/CIR/P/2020/136 dated July 24, 2020, further extended such timeline and the relaxations are now applicable for rights issue opening up to December 31, 2020.

|

|

Relaxations relating to procedural matters pertaining to takeovers and buy-back

|

|

SEBI had previously, vide circular dated May 14, 2020 granted certain one-time relaxations from enforcement of certain regulations of Takeover Regulations and SEBI...More

|

|

SEBI had previously, vide circular dated May 14, 2020 granted certain one-time relaxations from enforcement of certain regulations of Takeover Regulations and SEBI (Buy-back of Securities) Regulations, 2018 pertaining open offers and buy-back tender offers opening up to July 31, 2020. This update can be accessed from our earlier updates as provided here. SEBI has now, vide circular SEBI/HO/CFD/DCR2/CIR/P/2020/139 dated July 27, 2020, further extended such timeline and the relaxations are now applicable for open offers and buy-back through tender offers opening up to December 31, 2020.

|

|

Extension of time for submission of financial results for the quarter/half year/financial year ended 30th June 2020

|

|

SEBI had previously, vide circular dated June 24, 2020 extended the timeline for submission of financial results for the quarter/half year/financial year ending March 31, 2020...More

|

|

SEBI had previously, vide circular dated June 24, 2020 extended the timeline for submission of financial results for the quarter/half year/financial year ending March 31, 2020 by listed companies under Regulation 33 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“LODR Regulations”). This update can be accessed from our earlier updates as provided here.

|

|

Regulation 33 of the LODR Regulations requires a listed entity to submit its quarterly/half year annual financial results within 45 (forty five) days or 60 (sixty days), as applicable, from the end of each quarter/half year/financial year. Accordingly, listed entities are required to submit the financial results for the quarter/half year ended June 30, 2020, on or before August 14, 2020.

|

|

SEBI has now, vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/140 dated July 29, 2020 extended the timeline for submission of financial results by listed entities for the quarter/half year/financial year ended June 30, 2020 to September 15, 2020.

|

|

Clarification on applicability of Regulation 40(1) of LODR Regulations

|

|

SEBI vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/144 dated July 31, 2020 has provided clarification on the applicability of Regulation 40(1) of the LODR Regulations, which states that...More

|

|

SEBI vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/144 dated July 31, 2020 has provided clarification on the applicability of Regulation 40(1) of the LODR Regulations, which states that “..except in case of transmission or transposition of securities, requests for effecting transfer of securities shall not be processed unless the securities are held in the dematerialized form with a depository.”

|

|

Investors expressed concern that due to the above provision they have not been able to participate in open offers, buy-backs and delisting of securities of listed entities since the securities held by them were not in dematerialized form. Accordingly, SEBI has now clarified that shareholders holding securities in physical form are allowed to tender shares in open offers, buy-backs through tender offer route and exit offers in case of voluntary or compulsory delisting.

|

|

Use of digital signature certifications for authentication/certification of filings/submissions made to Stock Exchanges

|

|

SEBI had previously, vide circular dated April 17, 2020 permitted the use of digital signature certifications for authentication/certification of filings/submissions made under the LODR...More

|

|

SEBI had previously, vide circular dated April 17, 2020 permitted the use of digital signature certifications for authentication/certification of filings/submissions made under the LODR Regulations, to the Stock Exchanges, till June 30, 2020. SEBI has now, vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/145 dated July 31, 2020 extended the timeline for using digital signature certifications till December 31, 2020. This circular is applicable for filings/submissions made from July 1, 2020.

|

|

Procedural Guidelines for Proxy Advisors

|

|

Regulation 24(2) read with 23(1) of SEBI (Research Analyst) Regulations, 2014 mandates proxy advisors to abide by Code of Conduct specified therein. SEBI vide circular...More

|

|

Regulation 24(2) read with 23(1) of SEBI (Research Analyst) Regulations, 2014 mandates proxy advisors to abide by Code of Conduct specified therein. SEBI vide circular SEBI/HO/IMD/DF1/CIR/P/2020/147 dated August 3, 2020 (“Procedural Guidelines Circular”) has issued procedural guidelines which proxy advisors are also required to comply with. They are inter alia:

|

-

Proxy Advisors shall formulate the voting recommendation policies and disclose the updated voting recommendation policies to its clients. Proxy Advisors shall ensure that the policies should be reviewed at least once annually. The voting recommendation policies shall also disclose the circumstances when not to provide a voting recommendation.

-

Proxy Advisors shall disclose the methodologies and processes followed in the development of their research and corresponding recommendations to its clients.

-

Proxy Advisors shall alert clients, within 24 hours of receipt of information, about any factual errors or material revisions to the report.

-

Proxy Advisors shall have a stated process to communicate with its clients and the company.

-

Proxy Advisors shall share their report with its clients and the company at the same time.

-

Proxy Advisors shall clearly disclose in their recommendations the legal requirement vis-a-vis higher standard they are suggesting if any, and the rationale behind the recommendation of higher standards.

-

Proxy Advisors shall disclose conflict of interest on every specific document where they are giving their advice. Further, the disclosures should especially address possible areas of potential conflict and the safeguards that have been put in place to mitigate possible conflicts of interest.

-

Proxy Advisors shall establish clear procedures to disclose, manage and/or mitigate any potential conflicts of interest resulting from other business activities including consulting services, if any, undertaken by them and disclose the same to clients.

|

|

This Procedural Guidelines Circular was to be applicable with effect from September 1, 2020.

|

|

However, SEBI vide circular SEBI/HO/IMD/DF1/CIR/P/2020/157 dated August 27, 2020 has decided to extend the timeline for compliance with the requirements of the Procedural Guidelines Circular by 4 (four) months and will be applicable with effect from January 01, 2021.

|

|

Grievance Resolution between listed entities and proxy advisors

|

|

SEBI vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/119 dated August 4, 2020 has provided for grievance resolution between listed entities and proxy advisors...More

|

|

SEBI vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/119 dated August 4, 2020 has provided for grievance resolution between listed entities and proxy advisors.

|

|

While acknowledging the role played by proxy advisors in enabling shareholders to effectively participate in corporate governance decisions, SEBI has also stated the probability that proxy advisors and listed entities may have different views on any agenda item of the listed entity leading to grievances.

|

|

Accordingly, in order to facilitate resolution of such grievances of listed entities against SEBI registered proxy advisors, SEBI vide the circular has stated that the listed entities may approach SEBI, who will examine the matter for non-compliance by proxy advisors with the provisions of the Code of Conduct under Regulation 24(2) read with Regulation 23(1) of the SEBI (Research Analyst) Regulations, 2014 and the procedural guidelines for proxy advisors issued vide the Procedural Guidelines Circular.

|

|

This circular was to be applicable with effect from September 1, 2020.

|

|

However, on account of the extension of applicability of the Procedural Guidelines Circular, SEBI vide circular SEBI/HO/CFD/CMD1/CIR/P/2020/159 dated August 27, 2020 has also extended the timeline for compliance with the requirements of the circular for grievance resolution, which will now also be applicable with effect from January 01, 2021.

|

|

Relaxation from default recognition due to restructuring of debt

|

|

Credit Rating Agencies (“CRAs”) recognize default based on the guidance issued vide SEBI circulars dated May 3, 2020 and November 1, 2016. SEBI had previously...More

|

|

Credit Rating Agencies (“CRAs”) recognize default based on the guidance issued vide SEBI circulars dated May 3, 2020 and November 1, 2016. SEBI had previously, vide circular dated March 30, 2020 provided for relaxation from recognition of default owing to moratorium permitted by RBI and lockdown due to COVID-19 pandemic. Thereafter, RBI vide Notification dated August 6, 2020 provided for a resolution framework for COVID-19 related stress.

|

|

SEBI has now, vide circular SEBI/HO/MIRSD/CRADT/CIR/P/2020/160 dated August 31, 2020 provided relaxation whereby if the CRA is of the view that the restructuring by the lenders/investors is solely due to COVID-19 related stress or under the aforementioned RBI framework, CRAs may not consider the same as a default event and/or recognize default. Appropriate disclosures in this regard are required to be made in the press release. This relaxation is up to December 31, 2020.

|

|

Amendment in provisions relating to record date of SEBI (LODR) Regulations, 2015

|

|

SEBI vide Notification dated 05th August, 2020 has amended the provisions of Regulation 42 of the SEBI (LODR) Regulations, 2015 to provide that the listed entity now shall intimate...More

|

|

SEBI vide Notification dated 05th August, 2020 has amended the provisions of Regulation 42 of the SEBI (LODR) Regulations, 2015 to provide that the listed entity now shall intimate the record date for the specified events to all the stock exchange(s) where it is listed or where stock derivates are available on the stock of the listed entity or where listed entity’s stock form part of an index on which derivatives are available.

|

|

Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) (Third Amendment) Regulations, 2020

|

| SEBI vide Notification No. SEBI/LAD-NRO/GN/2020/20 dated July 01, 2020 notified the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) (Third Amendment)...More |

|

SEBI vide Notification No. SEBI/LAD-NRO/GN/2020/20 dated July 01, 2020 notified the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) (Third Amendment) Regulations, 2020 to further, amend the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 which shall come into force on the date of their publication in the Official Gazette i.e. 01/07/2020. The amendments are made in Regulation 17(1) to insert that in case of indirect acquisitions where public announcement has been made, an amount equivalent to 100% percent of the consideration payable in the open offer shall be deposited in the escrow account. Further, in Regulation 17(3)(c), it has been provided that the deposit of securities shall not be permitted in respect of indirect acquisitions where public announcement has been made. Furthermore, under Regulation 18(11) in case, the acquirer is unable to make payment to the shareholders who have accepted the open offer within such period, the acquirer shall pay interest for the period of delay to all such shareholders whose shares have been accepted in the open offer, at the rate of 10% per annum.

|

|

Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) (Third Amendment) Regulations, 2020

|

|

SEBI vide Notification No. SEBI/LAD-NRO/GN/2020/21 notified the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) (Third Amendment) Regulations, 2020...More

|

|

SEBI vide Notification No. SEBI/LAD-NRO/GN/2020/21 notified the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) (Third Amendment) Regulations, 2020 to further, amend the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018 which shall come into force on the date of their publication in the Official Gazette i.e. 01/07/2020. Through this amendment, SEBI has inserted new regulation for “Optional Pricing in Preferential Issue” as Regulation 164B. This Regulation provides for the price of the equity shares to be allotted pursuant to the preferential issue shall not be less than the higher of the following: (a) the average of the weekly high and low of the volume-weighted average price of the related equity shares quoted on the recognised stock exchange during the twelve weeks preceding the relevant date, or (b) the average of the weekly high and low of the volume-weighted average prices of the related equity shares quoted on a recognised stock exchange during the two weeks preceding the relevant date and the pricing method determined in this regulation shall be availed in case of allotment by preferential issue made between July 01, 2020 or from the date of Notification of this regulation, whichever is later and December 31st, 2020.

|

|

SEBI issues circular on asset allocation of multi-cap funds

|

|

SEBI had previously, vide Circular No. SEBI/HO/IMD/DF3/CIR/P/2017/114 dated October 06, 2017, issued guidelines regarding categorization and rationalization of Mutual Fund Schemes...More

|

|

SEBI had previously, vide Circular No. SEBI/HO/IMD/DF3/CIR/P/2017/114 dated October 06, 2017, issued guidelines regarding categorization and rationalization of Mutual Fund Schemes. SEBI, has now, vide circular SEBI/HO/IMD/DF3/CIR/P/2020/172 dated September 11, 2020, decided to partially modify the scheme characteristics of multi cap funds across the large, mid and small cap companies and be true to label. In this regard, the circular has issued the following minimum investment criteria:

|

|

“Minimum investment in equity & equity related instruments -75% of total assets in the following manner:

|

-

Minimum investment in equity & equity related instruments of large cap companies - 25% of total assets;

-

Minimum investment in equity & equity related instruments of mid cap companies - 25% of total assets;

-

Minimum investment in equity & equity related instruments of small cap companies - 25% of total assets.”

|

|

All the existing multi cap funds shall ensure compliance with this circular within one month from the date of publishing the next list of stocks by Association of Mutual Funds in India (AMFI), i.e. January 2021.

|

|

Thereafter, SEBI, vide PR No. 46/2020 issued a clarification pursuant to the above circular that mutual funds have many options to meet with the requirements of the circular, based on the preference of their unitholders. Apart from rebalancing their portfolio in the multi cap schemes, they could inter alia facilitate switch to other schemes by unitholders, merge their multi cap scheme with their large cap scheme or convert their multi cap scheme to another scheme category, for instance large cum mid cap scheme. SEBI is conscious of market stability and therefore, has given time to the mutual funds till January 31, 2021 to achieve compliance with the circular, through its preferred route of which rebalancing of the portfolio is only one such route.

|

|

Cut-off date for Re-lodgement of Transfer Requests Shares

|

|

SEBI, vide circular SEBI/HO/MIRSD/RTAMB/CIR/P/2020/166 dated September 07, 2020 has set the cut-off date for re-lodgement of transfer deeds as March 31, 2021 for transfer of securities...More

|

|

SEBI, vide circular SEBI/HO/MIRSD/RTAMB/CIR/P/2020/166 dated September 07, 2020 has set the cut-off date for re-lodgement of transfer deeds as March 31, 2021 for transfer of securities held in physical form and this circular applies to transfer deeds lodged prior to April 01, 2019 and which were rejected/returned due to deficiency in the documents and the same may be re-lodged with requisite documents. SEBI has further clarified that the shares that are re-lodged for transfer (including those request that are pending with the listed company/RTA, as on date) shall henceforth be issued only in demat mode.

|

|

Automation of Continual Disclosures under Regulation 7(2) of SEBI (Prohibition of Insider Trading) Regulations, 2015 - System driven disclosures

|

|

SEBI vide circular SEBI/HO/ISD/ISD/CIR/P/2020/168 dated September 09, 2020 has, in lieu of Regulation 7(2) of SEBI (Prohibition of Insider Trading) Regulations, 2015...More

|

|

SEBI vide circular SEBI/HO/ISD/ISD/CIR/P/2020/168 dated September 09, 2020 has, in lieu of Regulation 7(2) of SEBI (Prohibition of Insider Trading) Regulations, 2015 (“PIT Regulations”), issued directions for implementation of system driven disclosures for member(s) of promoter group and designated person(s) in addition to the promoter(s) and director(s) of company. The system driven disclosures shall pertain to trading in equity shares and equity derivative instruments i.e. futures and options of the listed company (wherever applicable) by the entities. The system would continue to run parallel with the existing system i.e. entities shall continue to independently comply with the disclosure obligations under PIT Regulations as applicable to them till March 31, 2021.

|

|

The circular further provides the steps/process required to be taken for implementation in an annexure. As per the steps, the listed company (rather than the registrar and share transfer agents) is required to provide the Permanent Account Number (PAN) of Promoter(s) including member(s) of the promoter group, designated person(s) and director(s).

|

|

Thereafter, SEBI vide circular SEBI/CIR/CFD/DCR1/CIR/P/2020/181 dated September 23, 2020 has decided to use the procedure of capturing the PAN of the promoters from listed companies as mentioned in the annexure of the circular dated September 09, 2020 for disclosures under Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 too.

|

|

Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Third Amendment) Regulations, 2020

|

|

SEBI vide Notification No. SEBI/LAD-NRO/GN/2020/33 dated October 08, 2020, has further amended the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements)...More

|

|

SEBI vide Notification No. SEBI/LAD-NRO/GN/2020/33 dated October 08, 2020, has further amended the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015.

|

|

In a bid to improve transparency in sharing information, markets regulator SEBI has mandated all listed companies to make disclosures about their forensic audit reports to stock exchanges. The companies will now be required to disclose their final forensic audit report, other than the forensic audit initiated by regulatory or enforcement agencies, on receipt by the listed entity, along with comments of the management, if any. All listed entities will now have to maintain 100 percent asset cover, or asset cover as per the terms of the offer document, sufficient to discharge the principal amount at all times for the non-convertible debt securities issued.

|

|

The regulator has removed the framework that said maintenance of 100 percent asset cover will not be applicable in case of unsecured debt securities issued by regulated financial sector entities eligible for meeting capital requirements as specified by respective regulators.

|

|

Furthermore, the listed entities will have to promptly forward to debenture trustees a half-yearly certificate regarding maintenance of 100 percent asset cover, or asset cover as per the terms of the offer document, in respect of listed non-convertible debt securities, by the statutory auditor along with the half-yearly financial results. The submission of half-yearly certificates will be exempted only where bonds are secured by a government guarantee.

|

|

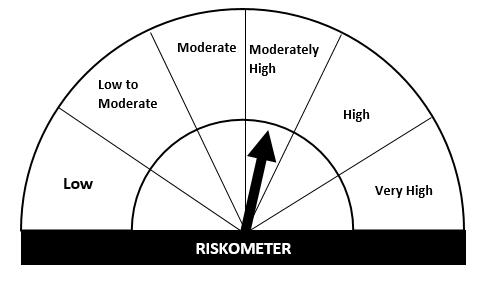

Product Labeling in Mutual Fund schemes – Risk-o-meter

|

|

SEBI, vide circular SEBI/HO/IMD/DF3/CIR/P/2020/197 dated October 05, 2020, has reviewed the guidelines for product labeling in mutual funds...More

|

|

SEBI, vide circular SEBI/HO/IMD/DF3/CIR/P/2020/197 dated October 05, 2020, has reviewed the guidelines for product labeling in mutual funds and decided:

|

|

|

a)

|

Risk Level of a scheme will be depicted by “Risk-o-meter”, as shown below:

|

|

|

|

|

|

|

b)

|

Risk-o-meter shall have following six levels of risk for mutual fund schemes:

|

|

|

|

-

Low risk;

-

Low to moderate risk;

-

Moderate risk;

-

Moderately high risk;

-

High risk; and

-

Very high risk.

|

|

|

c)

|

Based on the scheme characteristics, Mutual Funds shall assign risk level for schemes at the time of launch of scheme/New Fund Offer.

|

|

|

d)

|

Any change in Risk-o-meter shall be communicated by way of Notice cum Addendum and by way of an e-mail or SMS to unitholders of that particular scheme.

|

|

|

e)

|

Risk-o-meter shall be evaluated on a monthly basis and Mutual Funds/AMCs shall disclose the Risk-o-meter along with portfolio disclosure for all their schemes on their respective website and on AMFI website within 10 days from the close of each month.

|

|

|

f)

|

Mutual Funds shall disclose the risk level of schemes as on March 31 of every year, along with number of times the risk level has changed over the year, on their website and AMFI website.

|

|

|

g)

|

Mutual Funds shall publish the following table of scheme wise changes in Risk-o-meter in scheme wise Annual Reports and Abridged summary:

|

|

|

Scheme name

|

Risk-o-meter level at start of the financial year

|

Risk-o-meter level at end of the financial year

|

Number of changes in Risk-o-meter during the financial year

|

| |

|

|

|

|

|

|

This circular shall be in force with effect from January 1, 2021, to all the existing schemes and all schemes to be launched on or thereafter. However, mutual funds may choose to adopt the provisions of this circular before the effective date.

|

|

|

Review of Dividend option(s)/Plan(s) in case of Mutual Fund Schemes

|

|

The SEBI (Mutual Funds) Regulations, 1996 and SEBI Circular No. SEBI/IMD/CIR No 18/198647/2010 dated March 15, 2010 inter alia mandates that when units are sold, and sale price (NAV)....More

|

|

The SEBI (Mutual Funds) Regulations, 1996 and SEBI Circular No. SEBI/IMD/CIR No 18/198647/2010 dated March 15, 2010 inter alia mandates that when units are sold, and sale price (NAV) is higher than face value of the unit, a portion of sale price that represents realized gains shall be credited to an Equalization Reserve Account and which can be used to pay dividend.

|

|

There is a need to clearly communicate to the investor that, under dividend option of a Mutual Fund Scheme, certain portion of his capital (Equalization Reserve) can be distributed as dividend.

|

|

Accordingly, SEBI vide circular SEBI/HO/IMD/DF3/CIR/P/2020/194 dated October 05, 2020 has decided to stipulate the following:

|

-

All the existing and proposed Schemes of Mutual Funds shall name/rename the Dividend option(s) in the following manner:

|

|

Option/Plan

|

Name

|

|

Dividend Payout

|

Payout of Income Distribution cum capital withdrawal option

|

|

Dividend Re-investment

|

Reinvestment of Income Distribution cum capital withdrawal option

|

|

Dividend Transfer Plan

|

Transfer of Income Distribution cum capital withdrawal plan

|

|

-

Offer documents shall clearly disclose that the amounts can be distributed out of investors capital (Equalization Reserve), which is part of sale price that represents realized gains. Further, AMCs shall ensure that the said disclosure is made to investors at the time of subscription of such options/plans.

-

AMCs shall ensure that whenever distributable surplus is distributed, a clear segregation between income distribution (appreciation on NAV) and capital distribution (Equalization Reserve) shall be suitably disclosed in the Consolidated Account Statement provided to investors as required under Regulation 36(4) of SEBI (Mutual Funds) Regulations, 1996 and SEBI Circular No. CIR/MRD/DP/31/2014 dated November 12, 2014.

|

|

This circular shall be effective from April 01, 2021.

|

|

|

Rationalization of Eligibility criteria and Disclosure requirements for Rights Issues

|

|

SEBI by PR No. 51/2020 dated September 23, 2020 has amended the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 to rationalize eligibility criteria...More

|

|

SEBI by PR No. 51/2020 dated September 23, 2020 has amended the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 to rationalize eligibility criteria and disclosure requirements for Rights Issues’ with an objective to make the fundraising through this route, easier, faster, and cost-effective. The mandatory 90% minimum subscription would not be applicable to those issuers where the object of the issue involves financing other than the financing of capital expenditure for a project, provided that the promoters and promoter group of the issuer undertake to subscribe fully to their portion of rights entitlement.

|

|

SEBI has also allowed truncated disclosures for rights issues and now companies can file financial statements and periodic reports for last year instead of the last three years as required earlier. That is also applicable to cases where three years have passed after the change in management following the acquisition of control. SEBI has also increased the threshold to Rs 50 crore from Rs 10 crore for prospective issuers to file with SEBI the rights issue draft letter of offer for the regulator's observations.

|

|

Further, the issuer shall be eligible to make a fast-track rights issue in case of pending show-cause notices in respect to adjudication, prosecution proceedings, and audit qualification, provided that necessary disclosures along with the potential adverse impact on the issuer are made in the letter of offer.

|

|

Standardization of timeline for listing of securities issued on a private placement basis

|

|

SEBI, vide circular SEBI/HO/DDHS/CIR/P/2020/198 dated October 05, 2020 has decided to stipulate the following timeline within which securities issued on private placement basis under SEBI...More

|

|

SEBI, vide circular SEBI/HO/DDHS/CIR/P/2020/198 dated October 05, 2020 has decided to stipulate the following timeline within which securities issued on private placement basis under SEBI (Issue and Listing of Debt Securities) Regulations 2008, SEBI (Issue and Listing of Non-Convertible Redeemable Preference Shares) Regulations, 2013, SEBI (Public Offer and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 and SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015 need to be listed after completion of allotment:

|

|

Sr. No.

|

Details of activities

|

Due date

|

|

1.

|

Closure of issue.

|

T day

|

|

2.

|

Receipt of funds.

|

To be completed by T+2 trading day

|

|

3.

|

Allotment of securities.

|

|

|

4.

|

Issuer to make listing application to Stock Exchange(s).

|

To be completed by T+4 trading day

|

|

5.

|

Listing permission from Stock Exchange(s)

|

|

|

|

It was further decided that Depositories shall activate the ISINs of debt securities issued on private placement basis only after the Stock Exchange(s) have accorded approval for listing of such securities.

|

|

Further, in order to facilitate re-issuances of new debt securities in an existing ISIN, Depositories are advised to allot such new debt securities under a new temporary ISIN which shall be kept frozen. Upon receipt of listing approval from Stock Exchange(s) for such new debt securities, the debt securities credited in the new temporary ISIN shall be debited and the same shall be credited in the pre-existing ISIN of the existing debt securities, before they become available for trading.

|

|

In case of delay in listing of securities issued on privately placement basis beyond the timelines specified above, the issuer shall:

|

-

pay penal interest of 1% p.a. over the coupon rate for the period of delay to the investor (i.e. from date of allotment to the date of listing);

-

be permitted to utilise the issue proceeds of its subsequent two privately placed issuances of securities only after receiving final listing approval from Stock Exchanges.

|

|

The circular shall come into force with effect from December 01, 2020.

|

|

|

Utilization of Fund Created out of the Regulatory Fee Forgone by SEBI

|

|

In order to encourage the participation of Farmers/Farmers Producers Organizations (FPOs) in agricultural commodity derivatives markets, the Stock Exchanges have created a separate...More

|

|

In order to encourage the participation of Farmers/Farmers Producers Organizations (FPOs) in agricultural commodity derivatives markets, the Stock Exchanges have created a separate fund, out of the regulatory fee so forgone by SEBI. The Stock Exchanges have been permitted by SEBI to utilize the said fund exclusively for the benefit of and easy participation by Farmers/FPOs in the agricultural commodity derivatives market, in accordance with the guidelines specified vide SEBI Circular No. SEBI/HO/CDMRD/DMP/CIR/P/2019/40 dated March 20, 2019.

|

|

Due to low participation by Farmers/FPOs in agricultural commodity derivatives market coupled with the challenges posed by the pandemic situation, a sizeable portion of the fund has remained unutilized. Accordingly, SEBI has, vide circular SEBI/HO/CDMRD/DNPMP/CIR/P/2020/206 dated October 19, 2020 decided to permit the Stock Exchanges to utilize the said fund for the following additional activities:

|

-

Reimbursement of Mandi tax;

-

Reimbursement of assaying, cleaning, drying, sorting, storage and transportation charges;

-

Incentivising Option Premium; and

-

Reimbursement of fees levied by Clearing Corporation.

|

|

The Stock Exchanges can revise their action plan for utilisation of regulatory fee foregone by SEBI for FY 2020-21 incorporating the abovementioned activities and the revised plan, if any, shall be disseminated on their website. Further, in order to enhance transparency, the Stock Exchanges are advised to make disclosure regarding the corpus of the fund and its utilization, on their website, on a monthly basis.

|

|

The provisions of this circular shall be effective from the date of this circular.

|

|

AUTHORS

|

|

|

|

FIRM NEWS

|

| Link Legal adds Compliance practice after merger with S D Services... More |

|

Managing Partner, Mr. Atul Sharma in conversation with BW Legal World... More

|

|

Partner, Anuj Trivedi and Associate, Shreya Chaturvedi have contributed the India chapter for the second edition of the International Study on Foreign Investment Control... More

|

|

Webinar Recording | Session on Dispute Resolution - Arbitration, Mediation and Conciliation at India Infrastructure Forum 2020... More

|

| Agribusiness 2021 published by Lexology Getting The Deal Through... More |

|

A Dual Approach of Remedies for Home Buyers... More

|

|

The Arbitration and Conciliation (Amendment) Ordinance, 2020 No. 14 of 2020... More

|

|

Partner and Head - China Desk, Santosh Pai shares his expert views with BBC Correspondent, Faisal Mohammad Ali on the impact of India's exit from RCEP... More

|

|

Link Legal advised GMR Hyderabad Aerotropolis Limited on $80m GMR Hyd logistics park JV... More

|

|

Increased scrutiny of Chinese investment structures in India: An Analysis... More

|

|

Link Legal India Law Services partnered with National Law Institute University, Bhopal (NLIU) to organise the 3rd NLIU Link-Legal Client Counselling Competition 2020... More

|

|

Deciphering India's dependency on Chinese imports... More

|

|

|

AWARDS & RECOGNITIONS

|

-

Ranked highly in Construction, Energy, Infrastructure, Aviation, Banking & Finance, Banking & Financial Services, Restructuring & Insolvency, Corporate and M&A, Dispute Resolution, Capital Markets, Competition/Antitrust, Private Equity, Real Estate and TMT by Asialaw Profiles 2021.

-

Recognized in Project Finance, Capital Markets: Debt & Equity, Project Development: Infrastructure, Project Development: Power, Project Development: Transport, Restructuring and Insolvency and M&A by IFLR1000 2021.

-

Recognised as one the Largest Law Firms in India in Asian Legal Business' Asia's Top 50 Largest Law Firms list.

-

Ranked in Commercial and Transactions, Competition/Antitrust, Construction, Government and Regulatory, Insolvency and International Arbitration by Benchmark Litigation Asia Pacific 2020.

-

Ranked as one of the Top 20 Law Firms in India in the Venture Intelligence League Tables (Q3 2020) for M&A and Private Equity.

-

Ranked as one of the Top 15 Law Firms in India in the VCCEdge League Tables (Q3 2020) for M&A and Private Equity.

-

Ranked among Top Ranked Law Firms: Asia Pacific by Top Ranked Legal in Aviation, Banking & Finance, Competition/Antitrust, Corporate/M&A, Dispute Resolution.

-

Winner of ‘Utility Deal of the Year’ award at The Asset Triple A Infrastructure Awards 2020.

-

Winner in Aviation, Energy & Natural Resources and Infrastructure & Project Finance at India Business Law Journal’s 2020 Indian Law Firm Awards.

-

Infrastructure & Project Finance Law Firm of the Year by Legal Era Indian Legal Awards 2019-20.

-

Ranked #14 among Top 50 Indian Law Firms by RSG Consulting 2019.

-

Recognised as one of the 'Best Brands' at the Economic Times - Best Brands Summit 2019.

|

|

|

Disclaimer:

The contents of this newsletter are intended for information purposes only. Parts of this newsletter are based on news reports and have not been independently verified. The newsletter is not in the nature of a legal opinion or advice and should not be treated as such. Link Legal India Law Services does not warrant the accuracy and completeness of this newsletter, and readers are encouraged to seek professional advice before acting upon any of the information provided therein. In no event will Link Legal India Law Services be liable for any loss whatsoever arising out of the use of or reliance on the contents of this newsletter. This newsletter is the exclusive copyright of Link Legal India Law Services and may not be circulated, reproduced or otherwise used by the intended recipient without the prior permission of its originator.

|

|

|

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |